Better budgeting during Covid-19 is easier if you use the 50/30/20 budgeting technique. It’s really simple. But that doesn’t mean it’s always easy, especially if you’re on a reduced income.

The 50 bit relates to the idea that you don’t spend more than 50% of your money on life’s absolute essentials. Currently that might seem like too tough a target. You’re probably closer to 65%, i.e. for every £10 you earn – £6.50 goes on essential items like food and rent.

After essential spending there tends to be a bit of a three-way struggle between having some cash so you can live your life, paying down debt and saving for the future.

Under the 50/30/20 rule the idea is that around 20% of your income goes on financial commitments: paying off debt and saving.

If you’ve lost money because of Covid-19 – saving – never mind paying down debt, might seem unachievable. But that also makes it more than important than ever to practice better budgeting during Covid-19.

Thinking of borrowing?

It is natural to consider borrowing your way through a crisis. After all, that’s exactly what the government is doing.

If you have no savings, you could well end up putting some groceries on credit while waiting for your income to be topped up with tax credits and other benefits. Should you be thinking of putting a few things on a credit card… weigh up the cost (including interest) against the benefit.

Using up your limits on credit cards can also have a negative effect on your ability to get an affordable loan.

However, borrowing your way out of any financial difficulty, has a long-term cost.

The long-term cost of credit cards

Credit cards give you the option just to pay the minimum balance. Often this is between 3% and 5% of your outstanding balance. For every £100 owed you’d have to pay off between £3 and £5.

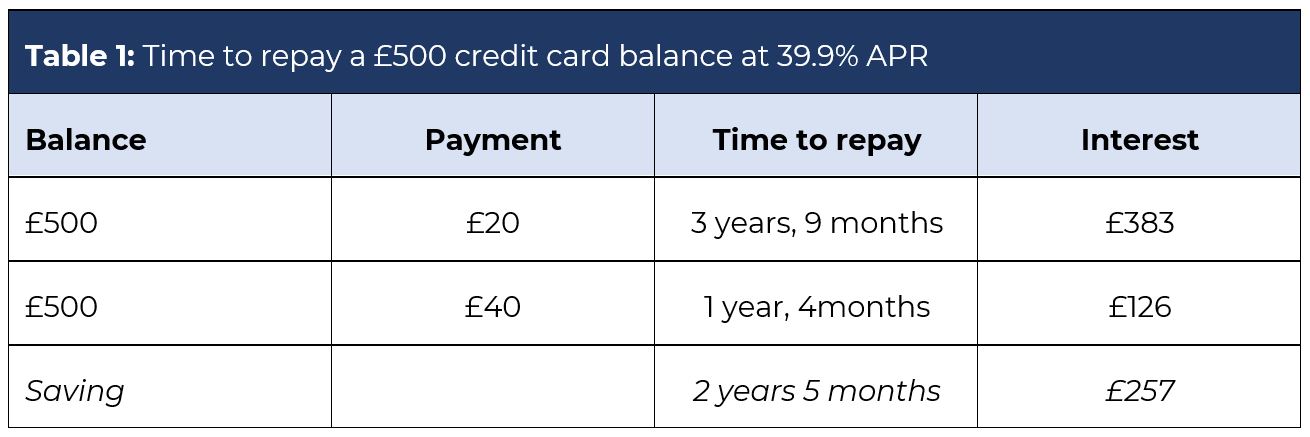

In the example below in Table 1, the minimum payment on a £500 credit card balance is 3% and therefore £15 per month.

Paying just little more than the minimum balance (£20) takes almost four years to clear the card. Furthermore – the interest charged is £383.

Doubling the payment to £40, clears the balance more than two years sooner.

Additionally, you would save you £257 in interest; over half of the original balance.

It seems logical that doubling the payment would halve the interest paid. But the benefit of making larger payments is greater. This is because credit cards charge interest on the daily balance. Consquently, the sooner you repay the less interest you’ll be charged.

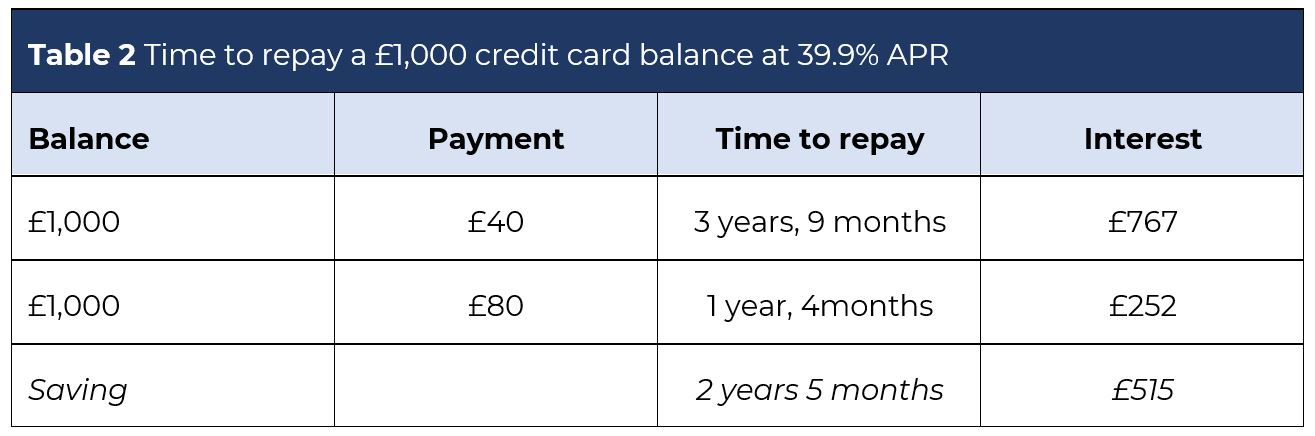

The cost of a higher balance

If you’re considering putting £500 of shopping on your card, think carefully about the cost. In the example below the balance inceases by £500 to to £1,000.

Even doubling your payment to £40 per month, would take almost four years to repay with £767 paid in interest.

In other words for every £1 you have spent on your card you’ve paid £1.67 back.

And most of what you’ve bought will be well past its sell by date if it takes nearly four years to repay!

Even increasing your payments to £80 means you’re paying £252 interest. That’s £1.25 for every £1 you borrowed.

Easier budgeting with the FREE NestEgg app

The NestEgg app will be available soon to help you budget better during Covid-19 and beyond.

Getting on top of your budget will make it easier to be accepted for affordable loans.

By securely connecting the app to your bank account using Open Banking it will identify ways for you to get the most from your money, pay down debt and start saving.

*****

Enter your email below to get an early invite for the app – as well as tips on financial health.